THIS MYTH—and it is decidedly and eminently provably a myth—is about as ingrained an economic/investing myth as ever existed. It ranks up there with the belief that federal debt is inherently bad (more in Chapter 13) as myths everyone believes—with their souls—no matter their ideology or creed. Every politician declares high unemployment is bad for the economy—and therefore the stock market. (But it’s never their fault! It’s always the fault of their opposition.) And politicians are united in their intransigent view that high unemployment causes economic weakness. Yet this is utterly backwards. Unemployment can be excruciating for the unemployed and their families, and we’d all prefer that everyone who wants a job could more easily get one. However, that doesn’t change the fact unemployment is now, always has been and always will be a lagging indicator. Said another way: Unemployment, high or low, is the result of past economic conditions, not a cause of future economic direction. We do not need low unemployment for the economy to grow, and high unemployment will not hinder economic growth going forward. Economic growth drives the need to hire, and a contracting economy drives the need to reduce headcount. All of this is easy to see if you think like a CEO would and not like a politician wants you to.

Pretend you are CEO of ABC Widgets, Inc. After four or five years of steady earnings growth, your revenues start falling. Slowly at first, so you think you can pull through. You start cutting costs—you tell your employees to telecommute instead of flying to meet new clients. You put off expansion plans. Sales start falling faster, and you cut costs more. Eventually, you recognize sales may not rebound fast. You’re not certain an official recession is underway—US recessions are always officially dated (by the National Bureau of Economic Research—NBER) after the fact. But you know what your business is doing, and based on what you hear from suppliers, vendors, etc., you’re concerned a prolonged downturn could be underway. You also realize you’ve cut costs all you can and now must turn to the last place employers like to cuts costs: employees. You hate doing it, but to keep the firm afloat, you must reduce headcount. Politicians never understand this, either. Employers hate cutting employees. They don’t do it frivolously. But if you don’t cut headcount, you could endanger the entire firm—and a bankrupt firm results in many more unemployed people. A firm that survives a downturn is one that can usually start hiring again, eventually. So you cut headcount. And maybe, after three or four or five tough quarters, your sales do tick up, just a bit. You’re well off peak sales volumes, but earnings are going in the right direction, in large part thanks to your cost cutting. Do you start hiring? No! Not unless you want your board to fire you! First, you don’t know if that sales increase was a one-time blip. Plus, your employees are handling your sales volume fine. Maybe better than fine—they’ve innovated new processes to make their lives easier with the reduced headcount. That’s the silver lining to recessions—many firms see huge productivity gains as remaining employees learn to make do with less. And those productivity gains are what let firms see huge earnings growth off even small top-line sales increases. A few quarters go by—but you still aren’t hiring. Revenues are improving but haven’t fully recovered. But you are turning a nice profit, which you aren’t rushing to spend in the event of that always-feared but rarely seen phenomenon: the double-dip recession. A cash cushion can help smooth out future bumps. Finally, you become more confident sales are on a sustained upward trajectory. Maybe NBER officially dates the end of the recession a few quarters back. But you still don’t rush into hiring full-time labor. Maybe you start with part-time or contract labor—cheaper to hire, easier to fire if things turn around fast. Finally, when you become convinced future sales could be imperiled if you don’t materially increase headcount, you start hiring full-time labor in a meaningful way. Seen this way, it makes sense that unemployment wouldn’t fall before a recession ends. Rather, it makes sense that unemployment might even rise and/or stay high for some time, even after the economy bottomed and started recovering.

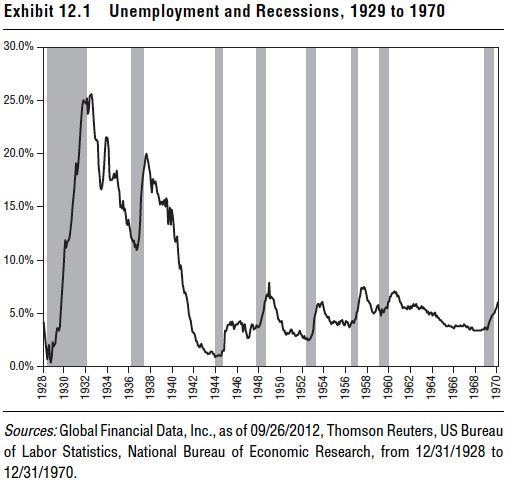

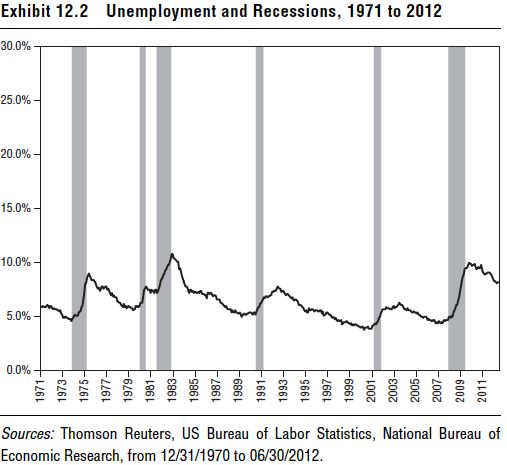

It’s not just theory. Exhibits 12.1 and 12.2 show historic unemployment rates and recessions. (I’ve split the historic data in two so you can really see how unemployment moves going into and out of a recession.) Through history, you see unemployment has never fallen before a recession ends. The reverse—it often rises after recessions and then stays high for many months or even years. This isn’t abnormal—it is normal and should be expected. It would be weird and contrary to economic fundamentals and actual history for unemployment to fall before a recession ends. Yet, politicians and pundits talk as if it should be so!

Pick up any newspaper, and you’d be forgiven for thinking low unemployment causes economic growth. If that were true, low unemployment would be a self-perpetuating growth machine. But that’s not the case. Recessions start, always, at or near cyclical unemployment lows. Which isn’t what would happen if low unemployment were an economic panacea. Rather, the data prove low unemployment doesn’t prevent recessions, and high unemployment doesn’t prevent economic growth. Being unemployed can be painful, but no matter the societal impact, that doesn’t change the fact economic growth begets lower unemployment, not the other way around. As an investor, you should care about unemployment’s impact (or lack thereof) on the stock market, too. Many similarly fear high unemployment is bad for stocks. But to believe that, you must misunderstand what stocks are and how they behave.

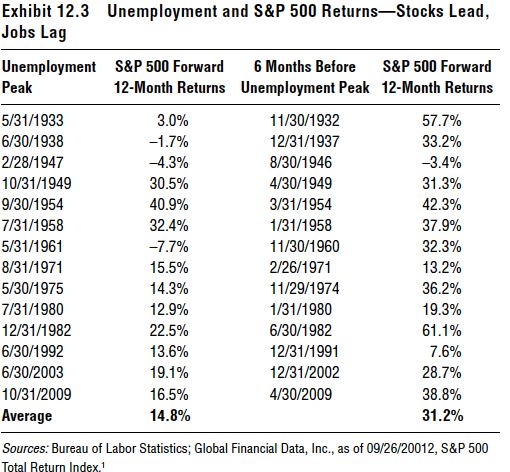

The stock market is the ultimate leading indicator for the economy—investors don’t wait for economic data to show economic recovery is underway; they bid up stocks ahead of time. So if stocks lead and unemployment lags, there’s no way unemployment, high or low, can be a material stock market driver. Don’t take it on faith: Check history. Exhibit 12.3 shows cyclical unemployment peaks and forward 12-month stock returns (using the longer history of US stocks). It also shows 12-month returns starting 6 months before the unemployment peak—i.e., when unemployment is still rising. Stock returns average 14.8% 12 months after an unemployment peak. Pretty great! But if you bought 6 months before the peak, your subsequent 12-month average return was a big 31.2%. Over double!

Don’t take this as a forecasting tool. You couldn’t time unemployment peaks (nor the point six months before) if you wanted to. I don’t know anyone who’s done it or even tried. But what this shows is stocks can and do rise when unemployment is high and rising. There’s no evidence high unemployment is a market negative. Just the reverse! Because unemployment is typically high as a recession is ending and just after. And stocks move first—and fast. (See Chapter 10.) It’s amazing this myth persists, particularly since there are ample data to check. So why does it? First, because folks don’t normally check if those things “everyone knows” to be true are actually true. It would be like doubting yourself, which we don’t like doing. And it would mean potentially feeling silly for falling prey to a myth—which we really don’t like doing. But second, in some ways, it might seem intuitive high unemployment would be economically bad. This is based on the idea consumer demand is a major driver of our economy. And it is, in a sense. Consumer spending accounts for 71% of GDP, now.2 But people misunderstand where the bulk of growth is coming from. If a lot of people are unemployed, that means they have less discretionary income to spend, which, following this logic, should ding the economy and ding stocks. Right? And yet, since the economy bottomed in 2009, consumer spending has steadily grown in the US and has been above the pre-recession peak level since December 2010.3 Yet, unemployment is still historically elevated! How can that be?

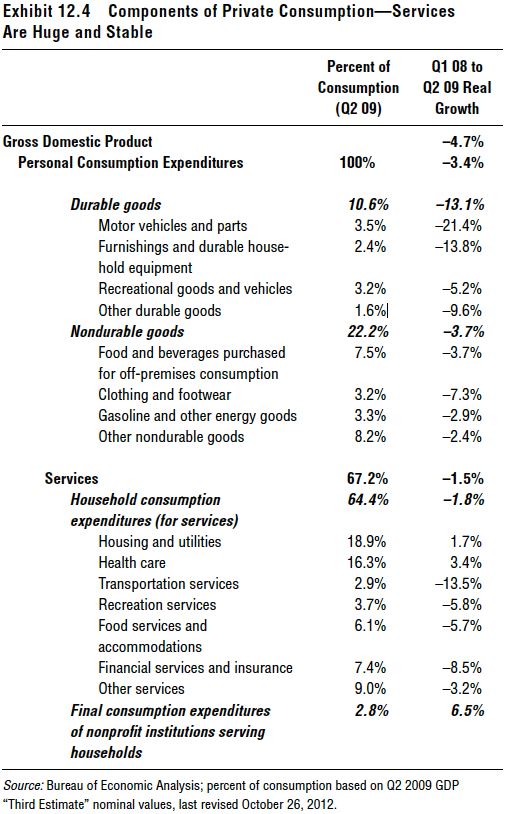

The truth is, US consumer spending is incredibly stable—it doesn’t shrink much in recessions so needn’t bounce back much in recoveries. That’s because much of what consumers buy is staples and necessary services. When times are tough, we generally still buy toothpaste and prescription drugs. And we spend on services like insurance, housing, utilities, etc. Maybe we switch from the fancy brand toothpaste to the generic, and maybe we’re more vigilant about using less heat, switching off lights, etc. But by and large, our average staple spending is pretty darn stable. Exhibit 12.4 shows the components of private consumption and how much they fell from the peak of real GDP growth in Q1 2008 to the trough in Q2 2009. And it shows how much of total spending each component comprised at the recession’s end. By far, the largest component of consumer spending (67.2%) is on services. During the 2007–2009 recession—which was steep by history’s standards—services spending fell just –1.5%. Spending actually increased on the two biggest services components: housing and utilities, and health care.

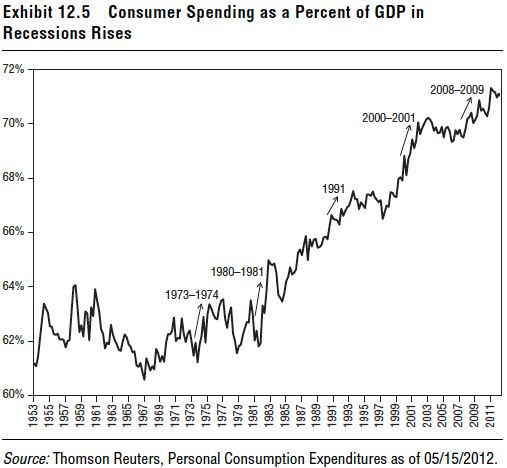

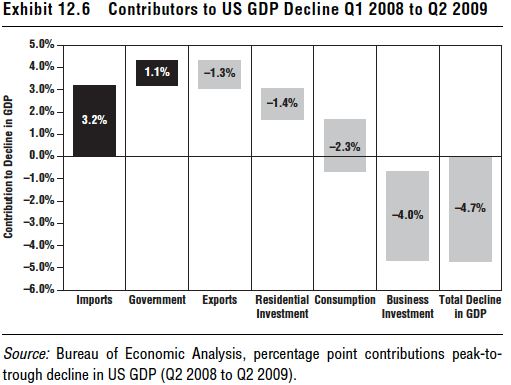

The next biggest chunk of consumer spending (22.2%) is on nondurable goods. Nondurables are things intended to last less than three years like shoes, clothing and groceries. These tend to be things you need more than you want, and this category fell just –3.7% peak to trough. Just 10.6% of spending is on durable goods. These are mostly (but not exclusively) big-ticket items. They comprise the smallest component, yet they’re the headline-grabbing items, i.e., “Auto sales fell 25%!” But is it so shocking that during a downturn, folks would put off buying a car, a washing machine or a flat-screen TV? That’s not great for those industries, but it’s not economically disastrous, either. Meanwhile, folks generally keep paying for basic necessities. Which is why, during the past few recessions, consumer spending as a percent of GDP has actually risen! (See Exhibit 12.5.) Yes, consumer spending does tend to fall a bit overall during recessions, but not as much as aggregate GDP. Business spending is a smaller but much more volatile component and is typically responsible for a bigger chunk of GDP’s rate change. Exhibit 12.6 shows the peak-to-trough contributors of major components of GDP during the 2007–2009 recession. (Though NBER dated the recession as starting in December 2007, output didn’t peak until Q1 2008.) Imports added to GDP, as did government spending, a bit.

Residential investment shaved off some output, but probably not nearly as much as most folks would think. Folks wrongly presume a weak housing market was the primary cause of the recession and 2008 credit crisis and bear market—but the reality is housing is too small a portion of GDP to have a very big impact. Consumer spending contributed –2.3%—not insignificant, but smaller than the –4.0% contribution from business investment. Had business spending been just flat, that would have been a mild recession indeed.

But, as mentioned, business spending is rarely flat in recessions. Recessions are recessions in large part because of the volatility of business spending. What’s more, businesses, i.e., producers, are the true drivers of economic vibrancy. Folks get this backwards, believing consumer demand is king. But if producers don’t produce, consumers can’t consume.

This isn’t a chicken-versus-egg debate. It’s simply the way the world works. If you don’t have entrepreneurs risking personal capital on a bet they can produce something the marketplace will like, you don’t get very much economic vibrancy. See it this way. It’s 2012 as I write. Just 15 years ago, maybe you had a cellphone, maybe you didn’t. Maybe it was a big clunky thing you’d be mortified to be seen with now. Did you know, 15 years later, huge swaths of humanity would be inseparable from their smartphones? That these tiny collisions of technology and consumer electronics would make your life easier? That you would get twitchy if you were separated from yours for more than a couple of hours? No! Someone invented first-generation smartphones—and they seemed like cool playthings for the super-rich and/or gear heads. Then the second generation came around. Then there were myriad copycats as technological advance collided with increased demand and production, driving down costs so they became economical for most anyone. Now they’re ubiquitous and being used in ways you never could have imagined 15 years ago. Heck, they’re being used in ways the original smartphone producers probably didn’t (and couldn’t) fathom. What decidedly did not happen was crowds’ banging down doors at their local electronics store saying, “Hey! I need a portable phone that’s also a computer, calendar and rolodex! It’d better use touch-screen technology, which is a thing no one has really heard of yet! Oh, and it absolutely must include a game where you catapult birds at buildings of wood, stone and ice in order to kill baby bird–stealing pigs!” Had you said such a thing, someone would have had you committed. No, innovative entrepreneurs, building on past innovations (see Chapter 1), invented smartphones, and the world decided it couldn’t live without them. And then cottage industries proliferated to design and deliver apps doing anything and everything you can imagine. And that’s how the economy really works. Without producers’ producing—whether they’re staples or discretionary goods or services—you don’t have much of an economy at all. Which is why folks get it so backwards when it comes to unemployment and the economy. Consumer demand isn’t the volatile driver of economic growth or lack thereof. It’s much too stable, even during periods of heightened unemployment. Producers are the major economic growth engines, and they want to take risk to produce something they think will lead to increased profits down the road. Politicians can rant and rave and wave blaming fingers all they like. But if they want unemployment to be lower, they should pass policies aimed at lowering barriers to entrepreneurship. It’s the growth that leads to the need for hiring, not the reverse. Never the reverse.