QUICK! WHEN I SAY, “Investment risk,” what comes to mind? Naturally and instinctively, for most readers, it’s, “Volatility!” Many investors act as though “risk” and “volatility” are interchangeable. And they often are! Volatility is a key risk that investors should consider (though, often, it can matter over what time period you consider volatility, as discussed in Chapter 1). And volatility is the risk that, most of the time and over shorter periods, investors feel most keenly. It can be heart-stopping to watch your equity allocation—whether it’s 100% of your portfolio or just 10%—lose up to 20% fast, as can happen in corrections. And even more grinding to watch it fall 30%, 40% or more in a big bear market. Ultimately, equity investors put up with volatility because finance theory says (and history has supported), long term, you should get rewarded for that volatility—more so than in other, less volatile asset classes. But volatility isn’t the only risk investors face. There are myriad! As discussed in Chapter 1, folks often believe bonds are safer. But there’s no universally accepted, technical definition of safe. And no bond is risk free. Bond investors face default risk—the risk the debt issuer delays payments or even goes bankrupt! It happens—even to highly rated firms. Default risk in US Treasurys is exceptionally low—so much so professionals often refer to it as the “risk-free” rate.

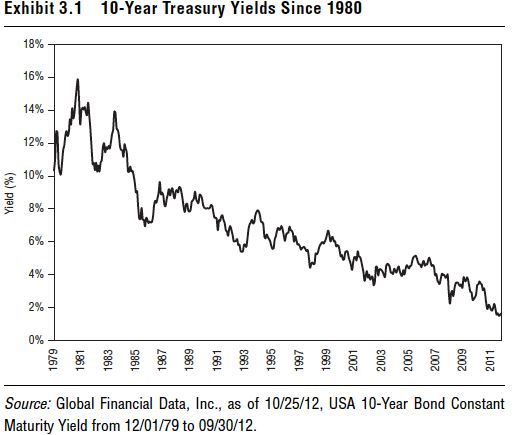

But that’s not exactly right. Why? There’s also interest rate risk—the risk interest rates’ moving in either direction impacts your return. In falling interest rate environments, investors may find it difficult to roll over funds from maturing bonds into something with a similar yield. If you bought a 10-year bond with a 5% coupon in 2003, your only option as it matures in 2013 is likely to accept a much lower coupon rate. Or if you want the 5% coupon, your option is likely a bond with a riskier profile or a longer term, which can also ratchet risk. Either way, it’s not an apples-to-apples rollover. That’s one half of interest rate risk. As I write in 2012, interest rates across the board are lower than they’ve been as long as most readers have been adults. Maybe lower than they’ve been in your lifetime! Exhibit 3.1 shows yields on 10-year Treasurys since 1980—rates have fallen with volatility nearly the entire time to generational lows. That rates are low doesn’t mean they must rise soon. They could bump along sideways. Heck, they could go a bit lower still. But, with 10-year Treasurys yielding under 2%, there’s not room for them to fall much. Still, at some future point, interest rates will rise again. I can’t say when or how fast. I rather doubt we see the sky-high interest rates we saw in the 1970s and early 1980s again—at least not very soon. Über-high rates then were the function mostly of disastrous monetary policy in the 1970s. Monetary policy in the US and most developed nations has overall improved since as we have more data and better communication and coordination.

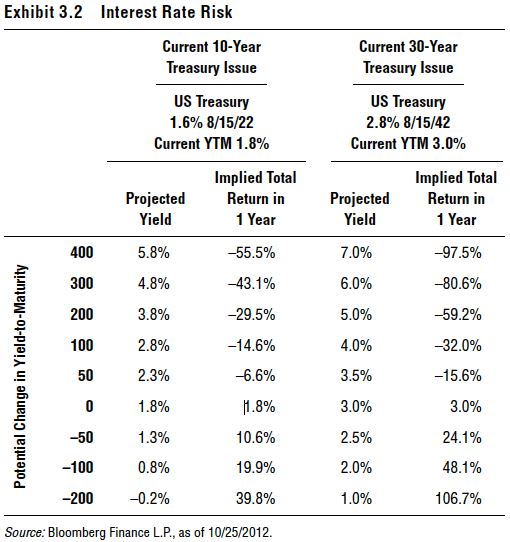

Though Ben Bernanke has made some pretty dumb moves. But even “Helicopter Ben” hasn’t been as bad as some of the past outright disaster Fed heads (ahem, Arthur Burns), though Ben still has time, and history will tell. If the market believes inflation will rise materially in the future, long-term interest rates will likely rise. But as goofy as Ben has been, I doubt we get a big enough spike in a short enough time to send 10-year rates from under 2% to above 10% very fast. So interest rates will rise at some point—which can erode the value of bonds you hold now. Some investors may say, “Yes, but I’ll hold my bonds to maturity.” Fine, you can think that, but 10 years is a long time. Thirty years much longer! And if you must sell, even a small interest rate move can seriously impact your return. Exhibit 3.2 shows the impact of rising interest rates on the value of 10-year and 30-year bonds. A 1% upward rate move wouldn’t be unusual in a year—that gives you an implied –14.6% annual return on your 10-year Treasury—not what you think bonds do. A 2% move is pretty big, but again, if interest rates are rising, some volatility wouldn’t be unusual. That would be an implied –29.5% return on the 10-year or –59.2% on the 30-year. The more interest rates rise, the worse the total return. That’s interest rate risk—don’t ignore it.

There’s inflation risk, political risk, exchange rate risk, liquidity risk. On and on and on. Volatility is decidedly not the only risk investors face. In 1997, I wrote a paper on risk with my friend and sometimes research collaborator Meir Statman (the Glenn Klimek Professor of Finance at Santa Clara University’s Leavey School of Business) titled, “The Mean-Variance-Optimization Puzzle: Security Portfolios and Food Portfolios,” published in the Financial Analysts Journal. Our research shows that the way people think about food and investing often parallels. In food, folks want multiple things at the same time. They don’t just want nutrition—they want food to look good and taste good. And they want to eat food at the right time of day. Cereal is a breakfast food—eating it at night is just sad. And diners want prestige! Packaging matters. What folks want from food can shift, fast. And what they feel as risk is what they want at a point in time that they think (or fear) they’re not getting. They don’t think about the things they are getting. For example: Maybe they’re forced to eat cereal at night—nothing else in the house. They don’t like that they’re eating something in the wrong order, and they feel foolish for it. Won’t admit it at work the next day! Those are two risks. They don’t think about the need that’s being fulfilled, i.e., basic sustenance. How does that relate to investing? As with dining, what folks feel as risk is often that which investors aren’t getting at a point in time—never mind if their other objectives are being met. You might hear investors say something like, “I don’t want any downside volatility!” They’re feeling volatility and want protection from it. Then, if stocks go on a long, sustained tear, they might feel like they’re missing out—and missing out is felt as another kind of risk.

That risk is called opportunity cost—the risk of taking or failing to take actions now that results in lower returns than you would have gotten otherwise. And it can be a killer. For example, you may have a longer investing time horizon, but perhaps you’re mostly concerned about shorter-term volatility and not any other form of risk. You may then choose to have too large a permanent allocation of fixed income than would otherwise be appropriate for your long-term objectives. Over your longer time horizon, because you don’t have enough exposure to equities, you likely get lower returns and increase the likelihood you miss your long-term objectives—maybe by a wide margin. That can hurt—a lot. Particularly if you’re depending on your portfolio to provide cash flow in retirement. If you’re planning on a certain level of cash flow, but your portfolio suffers from opportunity cost over a long period, you may find you must ratchet back your spending. What makes opportunity cost such a killer is its deleterious impact may not be obvious for some time. You may have a 20- or 30-year time horizon—or more! Twenty years from now, if you look back and discover you really needed to annualize 9% or 10% on average, but your lower short-term volatility portfolio yielded much less, that’s a massive portfolio error that may simply be beyond help. Twenty years of too-low returns is hard (if not impossible) to make up—particularly if you’re now taking cash flow. To reduce the odds you run out of money too soon, you may have to cut your spending. And that can be hard to do, even dispiriting, if you’ve been counting on a larger income—particularly if you’re already retired or nearing retirement—more so if your spouse was also counting on that income. That’s tough enough to take, and tougher still to explain to your spouse. And yet, most investors probably don’t think much about opportunity cost. Not normally. It tends to pop up as a broad concern after a bull market has been running for a while and usually coincides with extreme optimism or even euphoria. For example, in late 1999 and 2000, suddenly, investors everywhere were keen to chase the next big thing. The big returns of the 1990s made big equity returns seem easy—too easy. They wanted to ratchet risk—buy all hot Technology stocks! Oh, no! The opportunity cost of not day-trading hot recent Tech IPOs! And you know how that played out. But typically, investors default to focusing most on volatility and less (or not at all) on opportunity cost. Why is this very real risk often given second-class status? Warren Buffett popularized the saying, “You should be greedy when others are fearful and fearful when others are greedy.” Recall, for complex reasons rooted deep in the way our brains evolved over millennia, we tend to be hard-wired to fear losses more than we enjoy the prospect of gain. (See Chapter 1.) And by and large, investors tend to disbelieve bull markets as they run. Which is perverse! And yet, most readers of this book will agree that, overall and on average, investors tend to be bullish when they should be bearish and the reverse. So if stocks rise something on the order of 72% of all calendar years, folks are just going to be naturally bearish more often than not—and they’re going to downplay opportunity cost as a risk. Don’t do it. Volatility is a key risk, but not the only one. For many investors with long time horizons, not accepting enough volatility—opportunity risk—can be more devastating long term.