SOUND FAMILIAR? Have you said or thought that? Or heard someone say it? Plenty of investors think this way—whether it’s in the middle of a bear market, a correction or even during a normal bull market run when volatility kicks up a bit. But what is this normalcy folks are waiting for? A big “GET IN NOW!” sign? Or are they waiting for stocks to stop being so darn volatile and start appreciating in neat, tidy, non-panicky gradual-but-steady steps? Wait for that, and you’ll wait forever. The idea stocks will and should behave “normally” and give you an all-clear buy signal is pure myth. Stocks are normally volatile—sometimes more volatile, sometimes less, but volatile all the same. (Revisit Chapter 4.) And you want them to be. Sounds perverse, but it’s true. Finance theory is clear: You can’t get much return without risk (i.e., volatility). If stocks had lower shorter-term volatility characteristics, the returns would be lower over time. If you want better returns, you must accept a higher level of shorter-term volatility. If you want lower shorter-term volatility, you should expect lower returns. But this idea investors should wait until things seem more clear tends to pop up more frequently in the steep, painful bottoming period of a bear market—those days when stocks can swing wildly—maybe 4%, 5%, 6% or more in a single day! Yikes. Then, it can feel like waiting a bit until things are clearer—until you’re sure the bear market is over and the new bull under way—is a smart move. Maybe you’re already invested—stayed with the market throughout the bear. But the late bear market vicissitudes are wearing on you—and you’re scared there’s more to come. Should you bail, wait out the end and then get back in when the signs are clearer? (Another question: Are you that good a market timer? If so, why didn’t you time the top?) Or maybe you’re out and know you should get back in. But when? If you’re out, deciding to get back in can be incredibly hard—maybe harder than deciding to get out. Is it better to wait until it’s certain the bear market is over? No—clarity is one of the most expensive things to purchase in capital markets. That’s true whether it’s a bull, bear or any of the innumerable countertrend rallies within. And as counterintuitive as it seems, risk is actually least just when fear is highest and sentiment is most black—right as a bear market is bottoming. Clarity is almost always an illusion—a very expensive one. No one can perfectly time bear market bottoms. Sure, you can get lucky! But luck isn’t a strategy—it’s an accident. As painful as late bear market wild wiggles are in the shorter term, you don’t want to miss the start of a new bull market. New bull market returns are super-swift and massive—quickly erasing almost all late-stage downside volatility. Even if you suffer the last 15% to 20% of a bear market, it’s still almost certainly small compared to the subsequent initial up-leg of the next bull market.

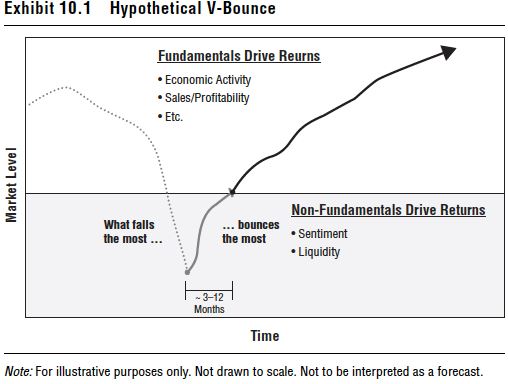

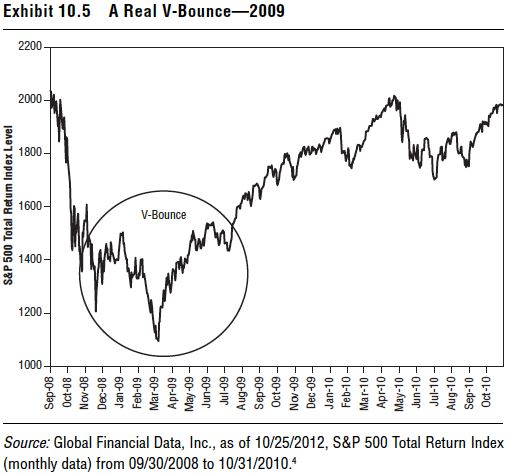

Exhibit 10.1 shows how a typical bear market works—like a spring. The more you depress it, the bigger the bounce. Sure, bear markets can (and often do) double-bottom, but that doesn’t diminish the bounce. And given enough time, W-bottoms resolve into more of a V.

When a bear market starts, deteriorating fundamentals drive the initial drop. Folks think bear markets start with a bang—they usually don’t. Corrections start like that—a big, sentiment-driven drop that scares the pants off most everyone. It would be much easier if bear markets had that pants-off scaring announcement factor. “Hey! Big bear coming!” But the reason so many people get ensnared is bull market tops tend to roll over, and the new bear slowly grinds lower. It doesn’t look or feel like a bear market—it feels like sideways choppiness, which happens during the course of bull markets, too! I call the stock market “The Great Humiliator” (TGH)—its aim is to humiliate as many people as it can for as long as it can for as many dollars as it can. And a favorite trick of TGH is to fool folks into a false sense of security with a rolling bull-market top. A sudden big bang effect would make it too easy for folks to see a bear forming and get out with minimal humiliation. It’s the latter portion where the bang happens. At a point, diminishing liquidity (like we saw in the fall of 2008 during the financial crisis) and sentiment take over from fundamentals. Panic often ensues. But panic is usually just sentiment and the temporary lack of liquidity that goes with the sentiment shift and is often confused with something fundamental. Stock valuations often become detached from reality. Which is why timing bear market bottoms is so devilishly tough. Sentiment is hard to gauge with any form of accuracy, anyway. And sentiment moves fast. Which is why, as a new bull market starts, the right side of the V-bottom can happen just as fast.

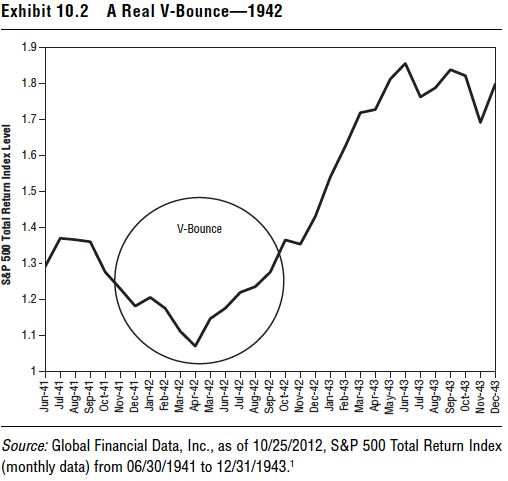

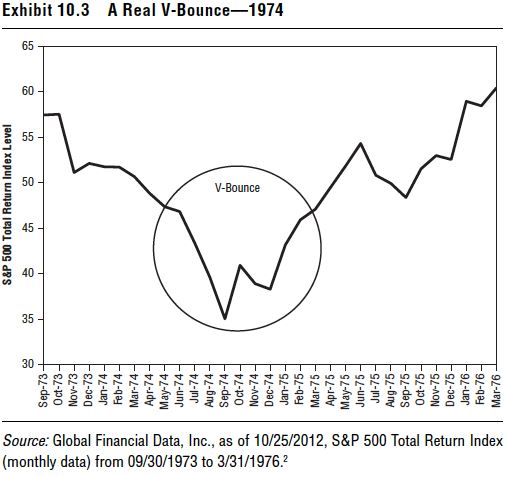

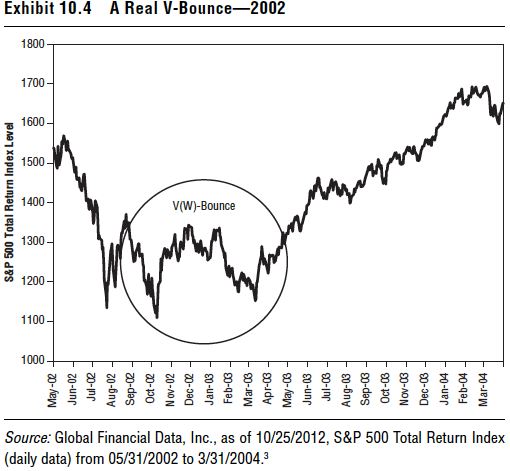

Folks often disbelieve new bull markets—often for years after they begin. But particularly in the early stages. “How can it be a bull market when everything is so bad?” they wonder. And everything probably is pretty bad. Bull markets often start before economic contractions bottom. But stocks don’t boom because things are improving. Rather, they boom because everyone expects Armageddon, but at a point, Armageddon doesn’t happen, and folks realize reality isn’t so dire. The panic was overdone. Just that slight sentiment melt on hugely depressed valuations can make stocks take off like a bullet. And the shape of the initial stage of the new bull market typically about matches the speed and shape of the end of the bear—what I call the “V-bounce” effect. (Another common V characteristic: In the late stages of a bear, when sentiment is driving big volatility, those categories that fall most tend to bounce most in the early part of the new bull. Read more on that in Chapter 19 of my 2010 book, Debunkery.) It’s not just theory—we see the V through history. Exhibits 10.2 through 10.5 show some of history’s V-bounces. Sometimes, bear markets end in more of a double-bottom W—with both bottoms a few months apart. And it can seem for a very short time like a W—but with minimal time, it resolves into a basic V pattern—and the bottom of the W portion begins to look tiny by comparison.

Missing those huge, early V-bounce returns while waiting for some illusory sense of “clarity” can mean missing your chance to erase a big portion of your prior bear market losses.

And it also hurts you relative to your benchmark. The ancestral part of our brains says, “Yikes! We fell a lot! Let’s protect ourselves so we can’t fall more!” If we act on that, it can make us feel better immediately—for a short while. But it can rob us of the huge returns we normally get from the early bull V-bounce. They may not undo all of the bear market, but they certainly put you on the way.

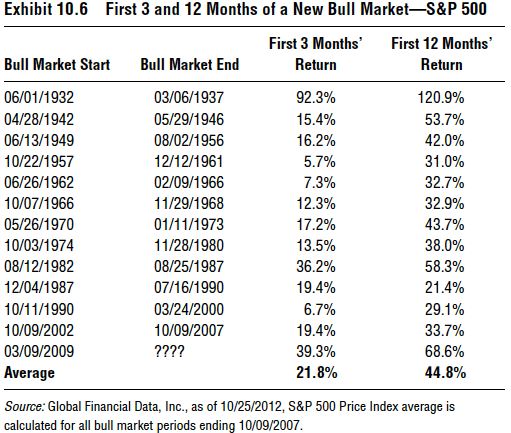

Volatility is huge on both sides of the V bottom. It’s only in retrospect you know which volatility you’re suffering through—late bear or early bull. But if you miss those early returns, you will regret it. Exhibit 10.6 shows how massive those early returns can be—averaging 21.8% in the first 3 months and 44.8% in the first 12 months! What’s more, the first 12 months are consistently big and fast—obviously some bigger and faster than others, but all big and fast nonetheless. A bull market’s average annual return is 21%5—but a bull market’s average first year more than doubles that!

And almost half those first-year returns usually (but not always) come in the first three months! And here, too, the market is tricky. Because on the occasions when the first three months aren’t so straight up, folks are prone to think it’s a sign the big boom will never come. This is just the market head-faking folks in another of its standard TGH humiliation tactics. Sometimes when the bottom is choppy on the left side of the V, it is also choppy on the right side, discouraging investors. But the V pretty much always works over a year.

Most all bull markets start this way—you can see it in history. Yet instead of a V (or W), people are usually instead looking for the agonizingly long-term L-shape. But I challenge them to find three examples of that ever in developed markets’ history. Only the onset of World War II in Europe knocked a global bull market off-course into a legitimate dragged-out L. A nascent bull market kicked off in 1938 but was truncated soon after the Nazis invaded the Sudetenland in 1939. Stocks didn’t finally bottom until 1942—and then surged in earnest. If you believe stocks won’t boom off the bottom, you better have a darned good reason to expect it. Only the threat of Nazis taking over the world with a communist Soviet overhang was enough to ever prevent a legitimate V-bounce. And all it really did was delay it—after the 1942 bottom, stocks formed the right side of the V. Stocks are resilient. That’s no myth.