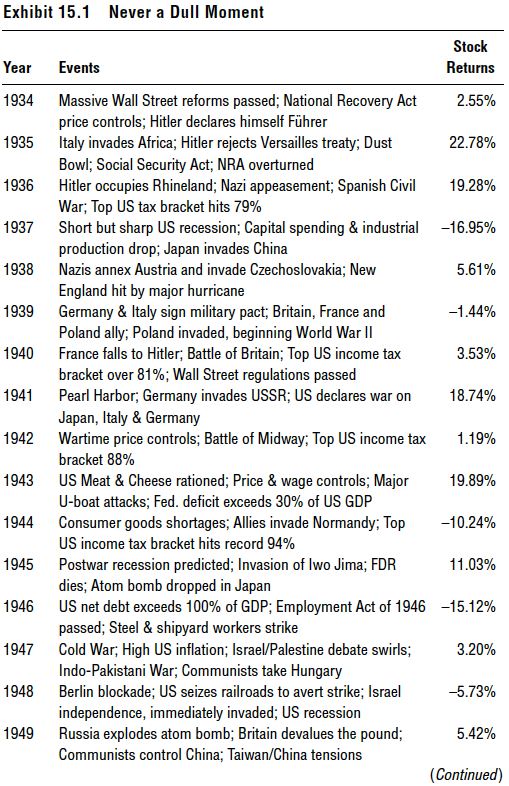

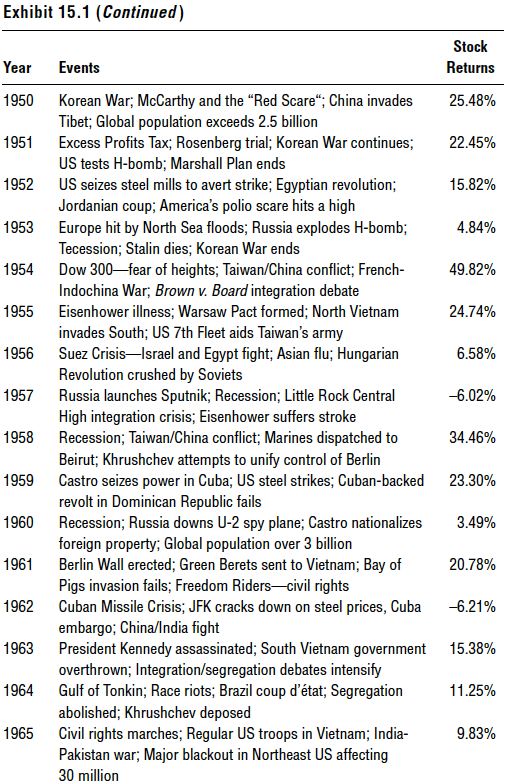

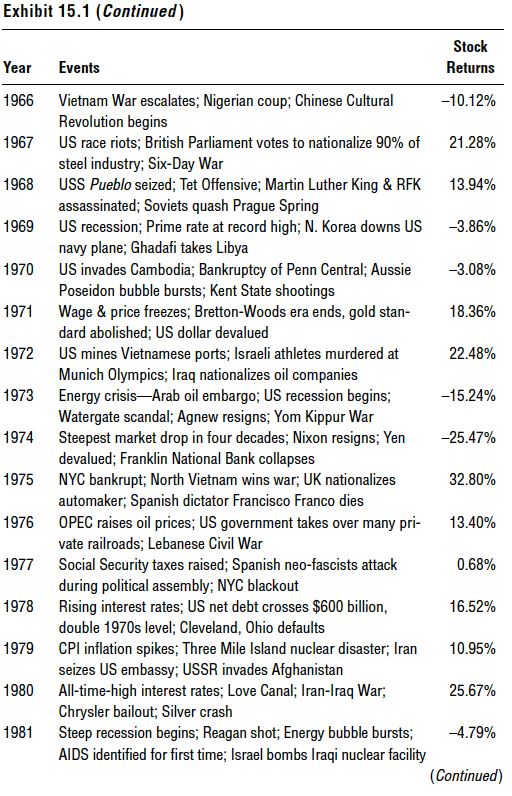

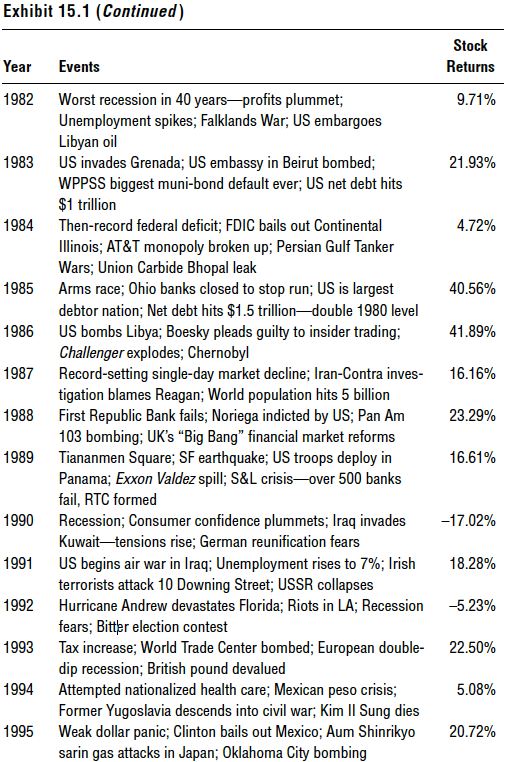

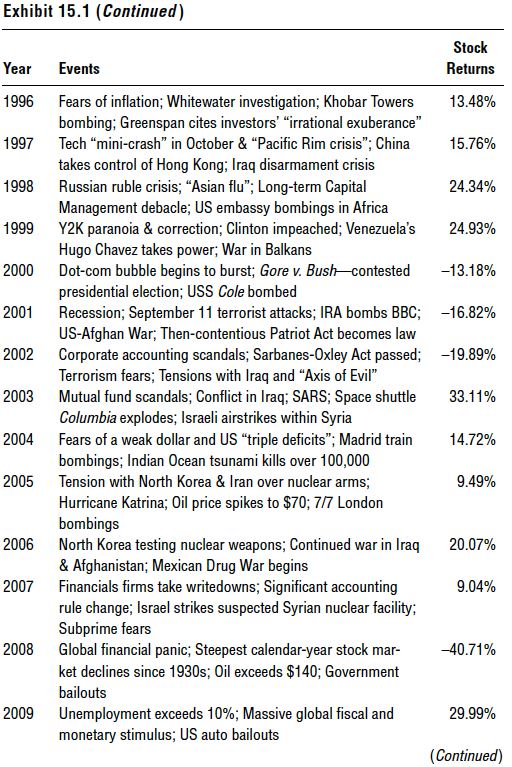

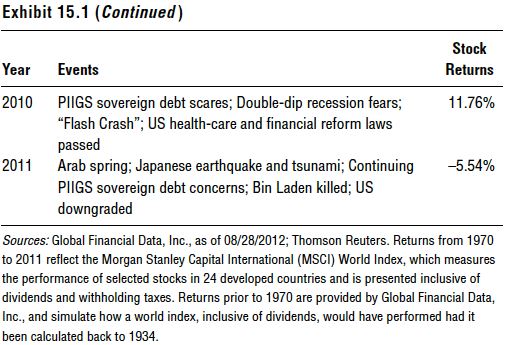

OFTEN, MEDIA AND PUNDITS tell us things are just “too scary,” the news too bad, the world too dangerous for stocks to rise. (More on how to better interpret media in Chapter 16.) Yet the world has always faced risks. Investors may say, “Yes, but that was then, and I always knew those past scary times would work out ok. But this time it’s different.” First, as discussed elsewhere in this book, folks always think this time it’s different. But it’s never so very different as folks fear. This is why Sir John Templeton famously said, “The four most expensive words in the English language are, ‘This time, it’s different.’” Among the jumble of evolutionary responses that helped humanity long ago but making investing tougher now: Humans evolved to forget past pain, fast. It was a survival instinct! We may think we were cool as cucumbers when faced with past fears, but the reality is, we very often weren’t. Think we’ve had a rough few years recently? A major Japanese earthquake and tsunami and nuclear accident. Heightened Middle East tensions. Contentious politics. But are politics truly more contentious now? Political rhetoric has always been heated—anyone who tells you we’re more divided now doesn’t know a shred of US history. Political infighting is a constant. (And if you think US politics are heated, you should watch a UK parliamentary session. Heck, in 2012, a male Greek politician punched a female political rival in the face on live TV.) Tensions have been flaring in the Middle East not just since Israel became a nation, but for all its history. (In 1801, the US Marines were dispatched to what’s now Libya to protect shipping lines from terrorists—the Barbary pirates.) And the world has been plagued by natural disasters since, well, the Big Bang. There’s no evidence natural disasters are increasing in frequency or ferociousness. Some folks like to claim even the weather is getting more severe and unpredictable for whatever reason, making hurricanes more fierce and such. Which doesn’t explain why the 1900 Galveston hurricane was the deadliest to ever make landfall on the US—and the second costliest based on inflation-adjusted dollars. Of the top 10 strongest US land-falling hurricanes, all but 2 were prior to 1970.1 The most active decade for hurricanes since we’ve been recording (in 1851) was the 1940s, with 24, followed by the 1880s with 22, and the 1890s and 1910s with 21 each.2 Why does that matter? Simply, folks inflate current events in their mind and misremember past events. Think geopolitics are tense now? What about for all of the Cold War? Or during the Cuban Missile Crisis, when missiles were actually aimed at our beds a short boat-ride away from Florida? Think debt is high now? It was well over 100% of GDP in World War II’s aftermath. Remember Chernobyl? That accident put Japan’s much better contained one in 2011 to shame. In the US, we’ve seen long periods of food rationing and gas rationing—not just in response to short-lived natural disasters. We’ve been hit on our own soil in Hawaii, New York and DC and had embassies attacked overseas (not just in 2012, but multiple times before). We’ve had oil shocks, strikes, recessions, riots, hyperinflation, deflation. Accounting scandals. Impeachments. Homegrown terror attacks on our own soil. Yet, look at Exhibit 15.1 which shows notable events for each year back to 1934 and annual global stock returns. Through it all, stocks have overall risen. Yes, bear markets occur, but no US or global bear market has ever been predicated by a natural disaster. Outside of the start of World War II in Europe, geopolitical tensions—even outright major terror attacks and the start of hot wars—have had a fleeting, and not necessarily negative, impact on stocks. History is never pristine. The world can be a pretty darn scary place—there’s never a dull moment. Yet, through it all, one constant is the resiliency of capital markets. If you’re waiting for things to “calm down” to be invested, you’ll be waiting a long time indeed. And if you didn’t invest during periods of turmoil, you wouldn’t spend much time invested at all—a mistake, since stocks have been up 72% of all years.3 How can stocks rise in the face of all this drama and trauma? Scary things are a constant in the world. Ones that are well known get priced into the market quickly. Their presence is just as often good, not bad, for stocks.

Then, too, remember that in the near term, stocks can wildly wiggle. But over time, their upward sweep represents the potentially infinite upward sweep of profits. As mentioned throughout the book, profit motive is an intensely powerful positive force. It’s at the root of capitalism and the reason free, democratic, capitalistic nations thrive and less-free nations don’t. Profit motive isn’t sapped because humanity faces challenges. In fact, challenges and the need for innovation can be motivating factors for those willing to take risks to chase future profits. Capital markets are resilient because humanity is resilient. Those who’ve bet against that have been proven wrong, time and again.