YOU WON’T FIND ANYONE who disagrees America is over-indebted. Societally, most just accept federal debt is bad—the bigger the debt, the bigger the bad. But remember, those things accepted without question are often those things most needing investigation.

Most people rationally understand that on a personal level, debt is ok. Some people get into trouble, which isn’t good. But most understand that debt, managed responsibly, is fine. In fact, necessary! Most folks couldn’t buy a house or a car without debt. Heck, most couldn’t buy a suit for that first job interview.

Most readers are probably also ok with corporate debt. Again, we understand some firms handle debt badly. But they have a major incentive not to—if they handle it really badly, maybe the CEO gets fired, which he/she doesn’t want. Maybe shareholders get mad and dump the stock. Or maybe the company goes bankrupt! All situations rational CEOs want to avoid.

But corporations often use debt to do things like build new factories, finance research or buy competitors or complementary businesses to expand. These things all help firms make or increase profits, and we like profitable companies. Profitable companies give us goods and services we want or need at a reasonable price. And they hire! All good things.

But this rational thinking tends to break down when it comes to government debt. We don’t like local government debt, and we detest state government debt, but our fiercest vitriol is reserved for federal debt.

Perhaps, rightly, many readers recognize governments are terrible stewards of your money—and the federal government is worse than the state, which is worse than the local government. All true! Governments are indeed very stupid, inefficient spenders of your money. Still, even the most ardent libertarian can agree we need roads and such. And the government establishes and enforces rules and regulations that protect both buyers and sellers, which is good. In my mind, perhaps the most important function of government is the fierce protection of private property rights.

I do wish the government spent less money. Not from any ideological standpoint, but just because I think you would spend it in much smarter ways that would benefit you and your family. And when you spend your money in self-interested ways, that’s ultimately better for society. If you don’t believe that, then you must not believe in capitalism. And if you don’t believe in capitalism, I’m not sure why you’re reading a book about stocks. But it was Adam Smith who said, “It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their regard to their own interest.” Which means, societally, we’re overall better off on average if, individually, we do what we view as best for ourselves. And you can do that better if you get to keep more of your money, the government less.

So I wish the government wouldn’t be such a stupid spender, but I don’t fear its debt—and neither should you. For reasons that follow.

First, people often say the US has “too much debt.” But that implies there’s some “right” amount of debt governments should have, and there’s a hard-and-fast line in the sand that, if crossed, becomes disaster.

Now, many would say the right amount of debt for a government is none. But that’s utterly unrealistic. I don’t know how a country could issue currency without a debt mechanism, or manage monetary policy. And for those thinking we could return to the gold standard, we still had federal debt when we were previously on the gold standard. What’s more, the gold standard didn’t protect against any form of economic ill. Bank panics were much more common and severe before the US established the Federal Reserve. The 2007–2009 recession was a walk in the park relative to the huge and frequent depressions of the 19th century.

What’s more, some argue a gold (or silver or bimetallic) standard takes meddling politicians out of monetary policy. This is the exact reverse of what would happen. It takes a huge amount of jiggering to set and then maintain a peg to a hunk of rock—jiggering by politicians. And once the rules are established, politicians can and will change the rules as they see fit. I don’t view America’s Fed as perfect. Far from it! But metal-based currency invites more government intervention, not less. (Nevermind the fact we would have to convince the rest of the world to go to a gold/silver/bi-metallic/whatever standard, and my guess is many nations would be inclined to tell the US to stuff it.)

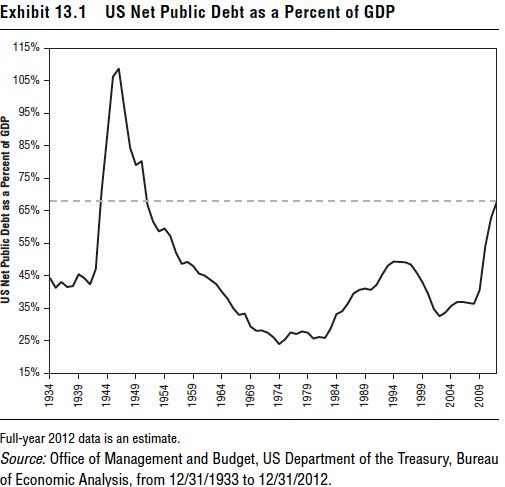

But there’s no evidence there’s a right debt level. What’s more, folks fail to put federal debt in perspective, instead citing debt in absolute terms. Exhibit 13.1 shows US net public debt as a percent of GDP, which is the right way to think about it. Net public debt is the total debt held by the public—it doesn’t include federal debt held by intra-government agencies, which can be thought of as federal IOUs. After all, when you do your household accounting, you don’t consider the 20 bucks you borrowed from your spouse a liability—it’s all in the family and in a sense cancels out.

US debt as a percent of GDP is currently elevated—which surprises no one. But it’s still well below peak levels. Debt hit 109% of GDP in 1946! But the period that followed isn’t remembered as a period of economic ruin. Rather, it’s remembered as a period of strong economic expansion and technological advance.

Some would argue it’s different now (always a dangerous assumption)—that was war debt. Sure. Except debt doesn’t care about the reason it’s issued. It’s debt! It’s a contract. It just has to be paid back, whether it was issued for a noble cause (fighting Nazis) or a silly cause (propping up failing solar panel producers). There’s no evidence higher debt then was a proximate cause for economic ruin.

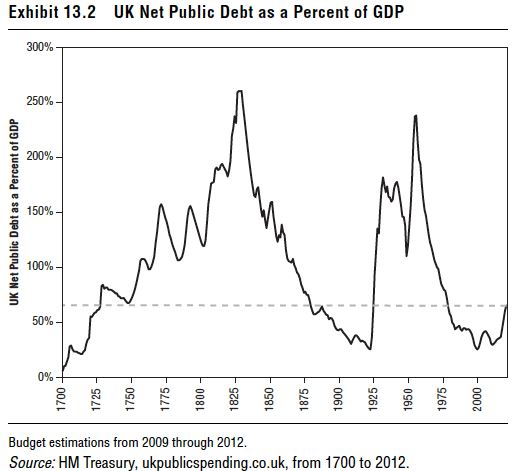

Then again, we have a relatively short data history to examine in the US. But that’s not true for the UK. Exhibit 13.2 shows UK debt as a percent of GDP, back to 1700.

Amazingly, the UK has had much higher levels of debt. Debt was above 100% of GDP from about 1750 to 1850, above 150% for about half that period and peaked above 250%!

Yet, what was going on in the UK in this period and after? Britain was the indisputable global economic and military superpower. The Industrial Revolution kicked off—earlier than in the US. The UK was the center for revolutionary manufacturing practices worldwide. All while it had major levels of debt.

And this was when news traveled by foot, horse, carrier pigeon and only much later by train. If the UK could survive as a superpower with debt above 100% for a century, there’s no reason America’s currently elevated debt must be long-term debilitating.

This may be hard for some readers to accept. Maybe the hardest myth in this book. Indeed, of everything I’ve ever written, this is the toughest concept for folks to get. The belief that debt is bad is so ingrained in us, most readers may just outright reject what I say, refuse to consider the data or contemplate the fundamentals—or they may just skip this chapter.

But why? Questioning what you believe—even if it’s something you deeply believe—doesn’t hurt. What’s the worst that can happen? You either find out you were right all along, which is fine. Or you find out you believe something that’s wrong that’s making you see the world all wrong and potentially leading to investing mistakes. Which is great! Because if you can see the world more clearly, you can make fewer mistakes and see greater long-term success. It’s win-win either way.

Now, many readers will also say, “But what about Greece? Don’t Greece’s big debt problems prove debt is bad?” No. It does prove socialism is bad. Greece doesn’t have a debt problem—it has a structurally uncompetitive economy thanks to decades of entrenched socialism. And it has a structurally corrupt government (thanks to the socialism) that makes it difficult to reform its ways to help make the economy more competitive going forward.

But Greece’s problem wasn’t the debt. Its problem was it had been cooking the books and got discovered. That, coupled with its uncompetitive economy, caused debt buyers to demand higher rates. They thought Greece wasn’t such a great credit risk anymore. And those higher rates made Greece’s debt interest payments very expensive.

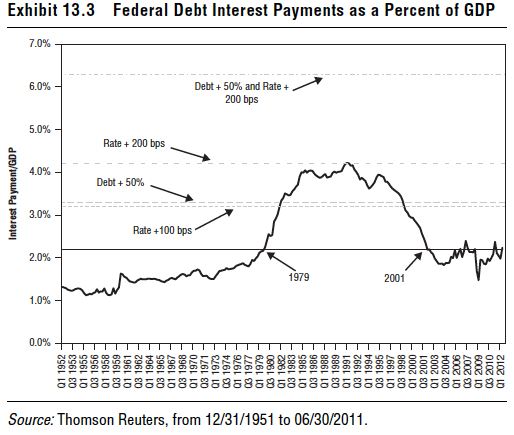

And that’s the crux of the problem. The issue isn’t debt, but whether that debt is affordable. And America’s debt is very affordable. Historically so! Exhibit 13.3 shows federal debt interest payments as a percent of GDP. Though our aggregate debt is higher now, our interest rates are very low—making the debt cheap.

As I write, debt interest costs are lower than the entirety of 1979 to 2001—not a period remembered for economic ruin. The reverse! For much of the 1980s and 1990s, the US was the dominant economic powerhouse. And the 1980s and 1990s featured two mega, near decade-long bull markets. Debt costs now are about half what they were from 1985 to 1995! Higher debt costs then weren’t problematic. Our much lower debt costs now can’t possibly be.

What’s more, either our aggregate debt amount or average interest rate paid or both must move hugely just to get to a level of debt interest payments that still wasn’t problematic in the past. First, higher interest payments would affect only newly issued debt, not existing debt. It would take some time for higher rates to materially move impact total interest paid.

Then, too, if average interest rates moved 100 basis points or total net public debt increased 50%, debt costs would still be below levels from 1982 to 1998—again, not alarming. If interest rates jumped 200 basis points, we’d just hit where we were in 1991—at the start of a massive economic boom and bull market. To get to levels never before seen, debt would have to increase 50% and interest rates would have to jump 200 basis points. I doubt that happens soon or fast.

Some may argue increasing debt would make interest rates rise because investors would lose faith. Again, where’s the evidence? America’s net debt level has been increasing the last few years, yet interest rates have fallen.

In fact, America’s debt rating was downgraded—and interest rates are lower than before!

For a brief refresher, in August 2011, in the wake of a rancorous debate over raising the US debt ceiling (an arbitrary marker that’s been raised over 100 times since it came into existence in 1917 to ease the war-funding effort), S&P downgraded the US from its pristine AAA rating. Folks were fearful that would kick off a crisis of confidence in US debt.

Didn’t happen. It was the reverse! US stocks, amid a correction, rallied through year-end 2011 and beyond. As I write in 2012, US stocks are strongly positive for the year.

And a year after the downgrade, across the board, Treasury rates were lower than they were. This is exactly opposite of what you’d think would happen if the world believed the US a worse credit risk.

But that’s just it. The world doesn’t think the US is a worse credit risk. That’s what the market is telling us. And in fact, S&P doesn’t necessarily think it is, either! Its downgrade was based not on fiscal or economic factors, primarily, but on politics. In S&P’s opinion, America’s two major political parties were unlikely to agree on major budget items. (Why it was news to S&P that politicians can’t agree is utterly mystifying to me. But never mind.)

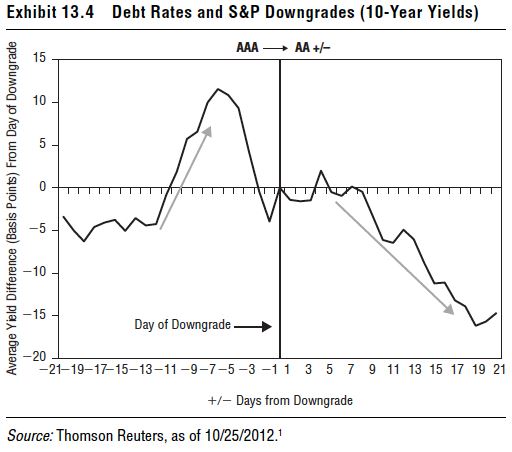

But if you checked history, this shouldn’t surprise you. There have been 12 instances when nations have been downgraded from an AAA status (S&P’s highest credit rating): Belgium, Ireland, Finland, Italy, Portugal and Spain in 1998; Japan in 2001; Spain and Ireland again in 2009; the US in 2011; and France and Austria in 2012. Exhibit 13.4 shows what happened to benchmark 10-year rates on average in the lead-up to and immediate aftermath of the rating cut.

It’s common to see yields spike just a bit right before the rating cut as markets price in fears of the coming cut. But the average spike is 11 basis points—not a huge move. And after the cut? On average, rates fall.

Why do markets tend to shrug off credit downgrades to AAA nations? The big three credit ratings agencies (S&P, Moody’s and Fitch) are effectively a government-backed oligopoly. Hence, as of now, the raters needn’t compete on price or quality. The market usually knows their opinions aren’t worth much.

What’s more, the raters have a knack for telling us what we already know. And if you base an opinion on the behavior of politicians—politicians who may not be around after the next election—the market has even less reason to care.

Fact is, the US may not be AAA in S&P’s eyes, but it still has the world’s biggest and deepest credit markets. Which is why America’s debt costs are manageable and likely to be for some time.

Maybe you buy into that notion—that our ability to afford our debt matters as much as (or more than) relative debt loads. But what about the common fear America is beholden to foreigners?

The story goes: Foreign countries prop up our profligate ways, and we’re dangerously beholden to them. Worse, China owns nearly all our debt! (Why China bugs people so much is beyond me. But whenever you read about foreign debt ownership, people make a big deal about China’s Treasury holdings. If the Chinese want to lend us money cheaply, I say let ‘em.)

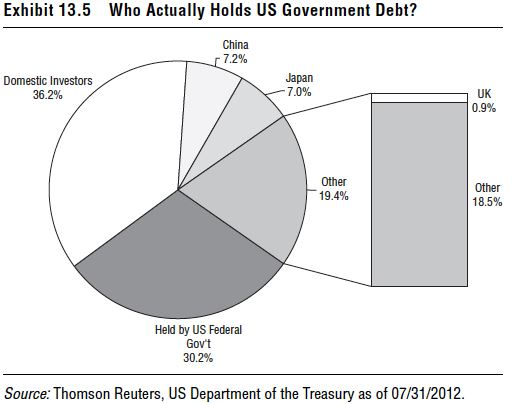

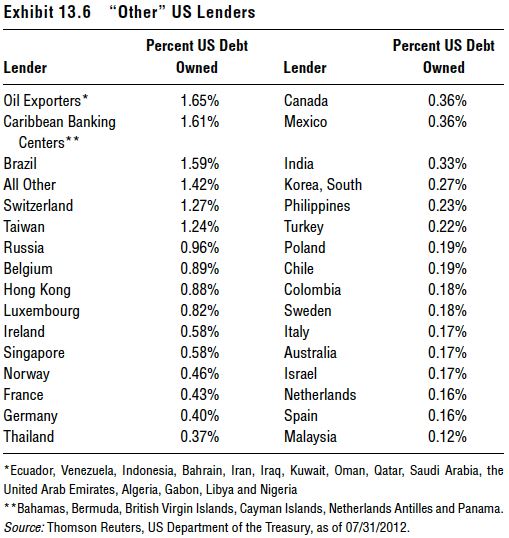

Is it true we’re dangerously beholden to foreigners? Exhibit 13.5 shows major holders of US debt, and Exhibit 13.6 breaks down the “other” category.

The largest chunk of our debt—36.2%—is held by domestic investors. Individuals, corporations, charities, banks, mutual funds and myriad other entities.

The US federal government itself owns 30.2% via intra-governmental agencies. Just 33.6% is held by foreign investors.

And it’s not all China. China holds a good chunk—7.2%. Hardly surprising since China is now the world’s second largest economy at about 11% of global GDP.2 Japan holds a near-identical amount—7.0%. But no one much complains about that. (Japan and China often flip-flop as America’s largest single foreign creditor.) In the 1980s, folks got kerfuffled over Japan’s economic growth and its purchase of US assets. But then Japan entered a long period of stagnancy—mostly because it doesn’t do capitalism right.

Folks who fear China’s overtaking the US in economic dominance should know China’s growth isn’t the organic growth of a free-market democracy. China’s communist government relies on fast growth to keep its urban citizens happy. It uses every lever available to create fast growth in the hopes educated citizens won’t notice (or will mind less) their rights’ being trampled. (This is a country where a billion people still live in subsistence poverty and a relatively few live in a style we’d call anything like “middle class” in the US.)

China may grow—a lot! Its output may even surpass the US at some point. But China needs more than rising output to challenge the US. Simply, China can’t surpass the US in economic dominance until it becomes a true, free-market democracy—which would be a great thing for China, the US and the world.

So Chinese and foreign investors in general don’t own scary-sized chunks of our debt. But folks tend to have two additional fears: that foreign holders will sell our debt, and that we won’t be able to repay them. And/or, they’ll stop buying our debt, and we won’t be able to fund our profligacy anymore. (If you believe we’re profligate. I don’t. I think the government is a stupid spender of your money, but I don’t worry about profligacy tied to the earlier point in this chapter about America’s debt being affordable.)

Run down this logic train: Why would it be scary if China (or anyone) sold huge chunks of our debt? That debt is a contract. If they want to sell it, there’s not some buy-back provision. We don’t have to fork over remaining principal all at once. Instead, China would sell its Treasurys on the secondary market. Someone else would buy the debt, and then we’d pay them the same interest rate we were paying China. No net impact on America there. We don’t care who’s holding the debt—we just care that we can make the interest and principal payments. (We can.)

But why would China want to dump a bunch of Treasurys at once? It would increase debt supply on the secondary market. Supply goes up, prices fall. China likely loses money on that trade, which is shooting itself in the foot.

But hang on—bond yields and prices have an inverse relationship. If China floods the market making prices fall, that makes interest rates rise—which makes our super-safe debt that much more enticing at the next auction to someone else! That increases demand, which would push prices up and yields back down. We don’t suffer much (if at all) in this scenario—which is unlikely because, again, like the butcher, baker and candlestick maker, China will act in its own best interest. And it isn’t in its best interest to dump a bunch of its US debt holdings all at once.

China isn’t buying US debt out of charity or some sense of global karma. It doesn’t feel obligated to the US. It buys our debt because it satisfies a particular need. In this case, China buys a lot of US debt to manage its currency, and because there aren’t any other debt markets that can accomodate China’s massive currency reserves.

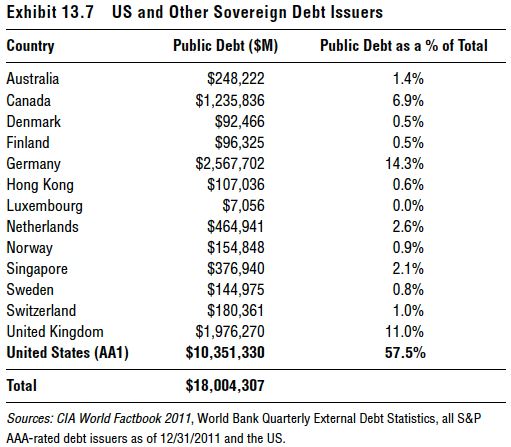

Then, too, if nations decide not to buy any US debt … whose debt will they buy? What other options have debt markets as deep? Exhibit 13.7 shows America’s net public debt relative to the remaining AAA nations—the likely substitutes for American debt. America’s debt is 57.5% of this group. Yes, China and the rest could buy Australia’s debt or Canada’s or Germany’s. And they already do! But they’d have to spread out their debt holdings considerably. Germany is the next largest low-risk issuer of government debt, but its public debt market is just 25% of America’s. There’s not a terrific full replacement for American debt, and it exposes investors to increased debt rate volatility.

America’s debt situation isn’t tenuous. We aren’t Greece. Not even close! And debt isn’t the inherent boogeyman so many believe. Debt, used wisely, is a right and normal part of a healthy economy. Avoiding all debt wouldn’t improve anything. There was a point in time when America had no debt—after Andrew Jackson paid off all of America’s debt in 1835 with proceeds from Western land sales. Which effectively led to the Panic of 1837 and the Depression of 1837 to 1843—one of the three worst recessions in America’s history (the other two started in 1873 and 1929).

Don’t fret the aggregate amount of debt. Focus on how affordable it is. And for America, debt is incredibly affordable and likely to remain so for some time.