THIS IS A MYTH MANY professional investors and hardcore enthusiasts tend to fall for—the belief that small-cap value is inherently better and prone to long-term superiority moving forward, forever and ever, world without end, Amen. It’s not true. Were it, we’d all know it, and everyone would invest in small-cap value, only. But there are also hard-and-fast (equally misguided) adherents to other equity size/style/categories. Some folks only buy large growth. Others buy only Tech. Only US. Only blue chips. Only British mid-cap Pharmaceuticals. Only this. Only that. Name a category, and there’s a fan group that believes it’s found the long-term silver bullet—its beloved category is best, no analysis needed beyond that. Yet no matter the depth of their love for [insert category here], they can’t all be right. And in fact, none are.

Another big feature of this perma-love: Often, it isn’t so permanent. Yes, some small-value disciples rigidly and adamantly hang on, even during the (sometimes, excruciatingly long) periods small value underperforms, so firm is their faith. But there are some who, after watching a category go on a tear for some time (large growth in the mid- to late-1990s, Tech in the late 1990s, Financials in the mid-2000s, foreign in the 1980s, US for all of the 1990s, Emerging Markets in the late 2000s, etc., etc., etc.), think, “Aha! This is the best category! I am missing out. But no more! I am convinced this category is best and will now shift heavily to it.” And they often shift in time for leadership to rotate (as it always does, irregularly), and they end up badly lagging. Maybe that hot sector crashes and they get crushed! And maybe they decide they were wrong (again) and go buy another category they see has been leading for some time and believe that’s the one that’s perma-better. This is pure heat chasing, nothing else. But they don’t think they’re chasing heat. No! We all know chasing heat is bad. Rather, they think they’re being rational. That the recent lengthy outperformance of Category X is evidence it’s just better. And sure, a particular equity category can outperform for a long time. But that doesn’t mean it’s permanently superior. It just means sentiment on that category was particularly strong, fundamentals justified its outperformance for a time or a combination of the two. But just because something has led for a long time doesn’t mean it must lead for a long time ahead. As an example, since 1926, small-cap stocks have annualized 11.9% to the S&P 500’s 9.9%.1 Proof small cap is perma-better? Not really. A lot of that outperformance ignores huge bid–ask spreads common in small-cap stocks in the 1930s and 1940s—sometimes up to 30% of the purchase price. If you actually bought and sold small-cap stocks then, costs ate up a major chunk of your return—but that’s not captured in long-term index returns. Then, too, small stocks tend to bounce huge off bear markets—the bigger the bear, the bigger the bounce. But that’s relatively short-lived. And small caps bounce huge because they fall huge in the later stages of the bear market—much more than the broad market. If you’re waiting for a huge small-cap bounce, you must also live through the huge small-cap plunge—super-emotionally tough. Outside just a few of the relatively hugest small-cap bounce periods, large caps overall beat small caps—and typically for agonizingly long periods. It can be mentally and emotionally trying investing in an asset style for which the relative payoffs are few and far between. And if you could perfectly time those bounces off bear market bottoms (hard to do), there are myriad other ways to make huge returns that beat small cap then. But those times when big stocks beat small are long enough to drive even the most patient investor absolutely insane. Most of the longest bull markets in history were dominated by big stocks.

Fact is, to believe a category is permanently and inherently better, you must disavow basic tenets of capitalism—primarily, that prices are set by constantly moving forces of supply and demand. In a basic college economics class, this probably was described to you as eagerness. How emotionally eager are consumers to buy (i.e., demand) something at varying prices? At higher prices, generally (but not always), consumers want less of something than at lower prices. Supply is about eagerness, too. How eager are suppliers to produce more or less of something at varying prices? Typically (but not always), producers will be more eager to produce something at a higher price than at a lower. At a point, consumer eagerness and producer eagerness meet—that’s your price. A price is an amazing technology. Folks don’t think about it that way, but a price is a simple manifestation of thousands, maybe millions, maybe billions of factors all colliding at a point where a buyer will buy and a seller will sell. (Politicians are forever wanting to tinker with prices, but that’s because politicians aren’t capitalists and cannot and will not ever understand the capital markets pricing mechanism.) Why did I say “but not always” twice? Sometimes, consumers do want something more at a higher price. The higher price might be part of the emotional package, tied to prestige or perceived quality or some other thing the buyer values. When Apple produces a next generation iPhone, for example, some folks wait in line to get the product the first day, even though the product is no different in three months and in six months, the price likely drops hugely. And sometimes, technological advances reduce costs for producers, making them more eager to produce at a lower price. (Basically, that’s Moore’s Law in action.) Still, this is all a reflection of varying levels of eagerness to consume or produce. Though media and pundits try to tie stock price movements to every imaginable factor, when you boil them down, stock prices, like everything else we buy in free markets, are driven by supply and demand. Near term, stock supply is relatively fixed. Initial public offerings (IPOs) and new stock issuances take tremendous time, effort and regulatory input—and they get announced well ahead of time. Cash- and debt-based mergers and share buybacks reduce supply but are also typically telegraphed ahead of time. Bankruptcies can also reduce supply but don’t happen in large enough volume to move the stock supply needle much. So over the next 12 to 24 months, you tend not to get big, unexpected stock supply swings. That’s when demand rules, driven largely by fickle sentiment—getting more positive or negative—which can happen fast. But longer term, supply pressures swamp all else. Stock supply can expand or shrink near endlessly over the long term in perfectly unpredictable patterns—increasing through issuances or shrinking through buybacks and cash- or debt-based takeovers. What happens is, one category starts getting more interest—like Tech in the late 1990s. Entrepreneurs and venture capitalists note that increasing demand and see investors willing to bid up values of that category—money seems easy to raise. They want in on that and the future profitability they think they can generate on relatively easy money. At the same time, investment bankers, whose societal purpose is to help firms access capital markets, also see growing demand in Category X. They help entrepreneurs by issuing new shares or new debt to raise money to launch a firm. Done right, this is profitable for all involved. Or maybe it’s not a new firm. It’s an existing firm that doesn’t want to miss out on potential profits from hot Category X. So it, too, issues shares or debt to raise money to start a new division or maybe buy another firm with expertise in that area. Or maybe it just wants capital to buy new equipment or do research or development. Business owners are happy to do this because they envision big future profits from their activity. Investors are happy to buy the shares because they want a piece of those future profits. And investment bankers are happy to help firms issue shares or debt because, again, it can be profitable for them. (Never forget the powerful force for societal good profit motive is.) The investment bankers keep printing new stock for new and established firms until, ultimately, supply swamps demand, and prices fall. Sometimes prices fall slowly, sometimes quickly—but demand falls and investment bankers don’t want to issue shares for the cold category as much anymore. They want to issue shares for the next hot (or even warm) category—increasing stock supply there. Meanwhile, excess supply in the now-cold category can get swept up as corporations buy back shares or go bankrupt or get swallowed by other firms. Supply can expand and contract endlessly and, in the long term, will overcome any major demand shifts. And because firms will always be motivated to raise capital at different points, and because investment bankers will always be motivated to help firms who need (or want) to raise capital by issuing shares to meet demand (or manage buybacks and takeovers for firms), future supply will always be unpredictable, but overpowering, in the longer term. Demand should float from category to category irregularly. There’s no fundamental reason why, 10 years from now, investment bankers should want to issue more shares of Tech versus Energy versus a larger category like small-cap or large. Each category—if well constructed—should travel its own path but net very similar returns over über-long periods, as the forces of supply ultimately drive long-term returns.

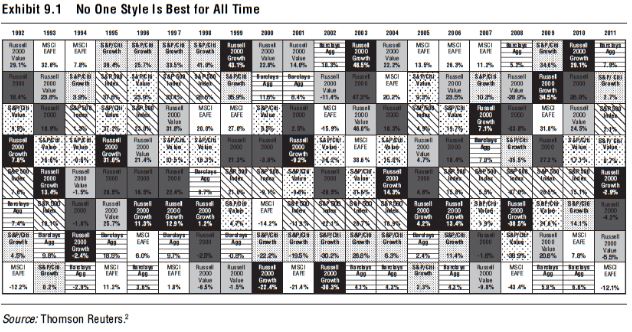

Another way to think about that is Exhibit 9.1, which looks like a crazy mish-mash quilt with no discernible pattern. It shows major asset classes (large-cap US, large-cap foreign, large US growth, small value, bonds, etc.,) and how they performed each year relative to other categories. So, in 1990, small-cap value did best, and foreign stocks (MSCI EAFE) did worst. The next year, foreign stocks did best! But the boxes move around. Buying last year’s winner didn’t result in next year’s winner, nor did being a contrarian and buying last year’s loser. Sometimes one style does best for a while and then gets buried. But no one box dominates, and there’s no predictive quality. Another key takeaway from Exhibit 9.1: If you don’t have a fundamental reason for favoring something other than it’s been hot, you’re probably just chasing heat. That may work for a bit from pure coincidence but isn’t a long-term winning strategy. In fact, it’s more likely a long-term losing strategy. Don’t fall in perma-love. Love is just another form of bias, blinding you to reality.