HUMANS LOVE SHORT-CUTS. Even in investing! We want to believe there’s an easier way. Just look at the proliferation of “lose-weight-fast” gimmicks. And there are a million “get-rich-quick” schemes (which are mostly scams—more in Chapter 17). A popular short-cut in financial planning circles is the idea you can take 100, subtract your age, and that’s how much you should have in stocks. You can read that rule of thumb in magazines, blogs—even some professionals adhere to it. There are variations—some say “take 120.” (Already you should be skeptical of a rule of thumb with an inherent 20% swing in asset allocation depending on which one you follow.) This bit of investing non-wisdom persists because it seems simple. Concrete! Straightforward. It’s a fast and easy solution to the very serious issue of asset allocation. But be wary of anything regarding your long-term financial planning that seems fast and easy. More broadly, investing rules of thumb should be regarded with severe cynicism, if not ignored outright.

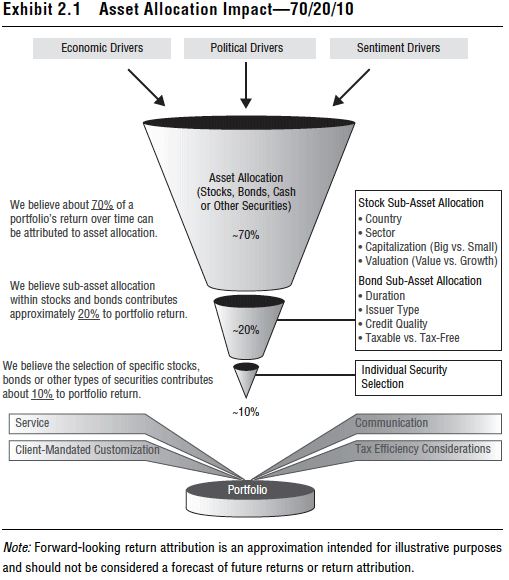

Long-term asset allocation decisions are, in fact, important. Most investing professionals today agree the long-term asset allocation decision is the most critical one investors make. Many point to an academic study that found about 90% of a portfolio’s return over time can be attributed to asset allocation—the mix of stocks/bonds/cash/other securities and in what percentages.1 At my firm, we take this a step further. You can think of it like the funnel in Exhibit 2.1. We believe 70% of portfolio performance is driven by the asset allocation decision—the mix of stocks/bonds/cash/other securities. We believe 20% of portfolio performance is driven by sub-asset allocation—the subsequent decisions on categories of securities—size, style, country, sector, industry, credit rating, duration, etc. The final 10% of performance over long periods on average is driven by the selection of individual securities, i.e., whether you hold Pepsi or Coke, Merck or Pfizer, an IBM bond or Microsoft, etc.

Either way, few argue the asset-allocation decision isn’t key for long-term success. So why would anyone relegate it to a simplistic rule of thumb? Folks who believe this believe age—and age alone—is the only factor that matters. One thing! That cookie-cutter way of thinking presumes everyone of a same age is identical. I can think of few rules of thumb more potentially injurious. This ignores things like investors’ goals, how much cash flow they may need now or in the future and how much growth is appropriate for their goals. It ignores current circumstances, portfolio size, whether the investor is still working or not. It ignores myriad more details unique to that investor. And it ignores the spouse! I’ve learned a tremendous amount in my long professional investing career—perhaps one of the more important lessons is never forget the spouse. That’s a good rule for your personal life, too. Yes, age matters. It figures into investing time horizon. But time horizon is just one factor that should be considered alongside and in concert with things like return expectations, cash flow needs, current circumstances, etc. (For more, see my 2012 book, Plan Your Prosperity.) This rule of thumb by definition ignores all that.

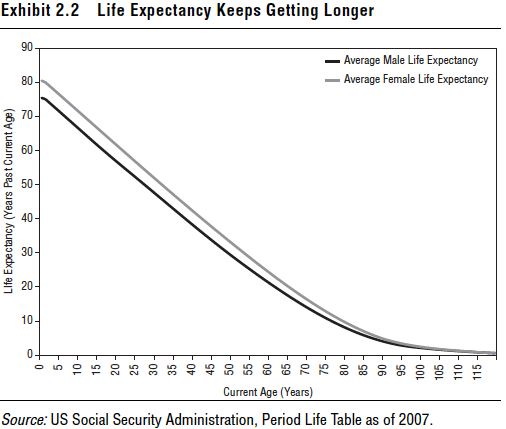

Even if I can get folks to stop thinking about age and start thinking about time horizon— and if I can get them to accept that time horizon is an important factor but just one and not the sole driving factor for asset allocation—much too often, folks think about time horizon wrong. Folks often think this way: “I’m 60. I plan to retire at 65, so I have a five-year time horizon.” They think of time horizon stretching out to retirement day, or the day they plan to start taking cash flow or some other milestone. To me, this form of thinking potentially cuts you off at the knees and leads to errors. Worse, those errors may not become apparent until years later—often too late to do much about them. Time horizon isn’t the period of time between now and some milestone. Time horizon is how long you need your assets to work for you. For many individual investors, this is often their whole life and that of their spouse. Never forget the spouse. Exhibit 2.2 shows average life expectancy, straight from the Social Security Administration’s actuaries. If you’re a 60-year-old man in the US, Social Security estimates your average life expectancy is another 21 years on average. If you’re a 60-year-old woman, your estimated average life expectancy is another 24 years. Is that your time horizon? Maybe. Do you think you’re average? If you’re in good health, active and have parents still alive in their late 80s, you could easily beat the odds—that could mean a 30-year (or more) time horizon.

Unless, for example, you’re a 60-year-old man married to a 55-year-old woman—also healthy and active. Her parents, both in their 80s, are still alive. And her grandparents died in their 90s—longevity is in her DNA. That’s a potential 40-year time horizon or more—depending on what your other goals are. If your goal is to pass as much as you can to children, you may want to think longer than 40 years. If your goal is to support just the two of you through retirement, think more along the lines of your own life expectancies. Could both of you die earlier, thwarting your planning? Of course. But dying with ample money in the bank isn’t a function of bad planning. What you don’t want to do is plan for a 25-year time horizon, get to 85 and discover the money has largely run out. You won’t enjoy that. And if your spouse lives to 95, he or she really won’t enjoy that—aged poverty is cruel.

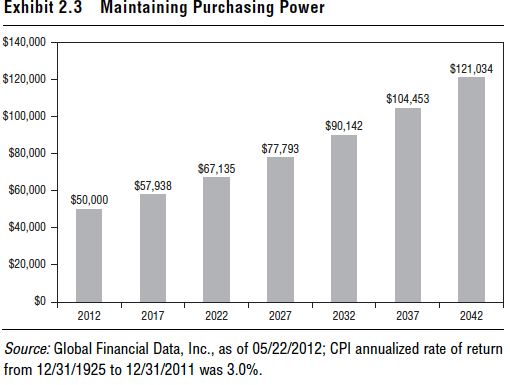

One of the bigger mistakes investors make is underestimating their time horizons and failing to plan for enough growth to accomplish their goals. Many investors assume they don’t have big growth goals but fail to remember (1) inflation’s insidious impact, and (2) inflation doesn’t impact all categories equally. Over time, inflation can take a serious whack at your purchasing power. Say you need $50,000 today to cover your living expenses. In 10 years, if inflation is anything like its long-term historic average (about 3% annually),2 you’ll need over $67,000. And in 20 years, you’ll need $90,142. (See Exhibit 2.3.) If you’re a 60 year old in good health, living another 30 years is certainly possible. If you’re 50, living another 30 would be unremarkable. To maintain the purchasing power of your $50,000, in 30 years, you’ll need $121,034! If you’re relying on your portfolio to kick off all or part of the cash flow needed to cover living expenses and you have a long time horizon, you likely need some growth, just to increase the odds your portfolio stretches enough so your cash flow keeps pace with inflation. By underestimating your time horizon and underestimating how much growth you need, you could increase the odds your portfolio is unable to kick off the level of cash flow you had been counting on. And if you discover that 10 or 20 years down the road, you may not be able to do much about it.

Then, too, you want to assume a life expectancy a bit on the long side and, therefore, your time horizon (if your time horizon is driven by your life expectancy and/or that of your spouse). Why? Life expectancy keeps expanding! In every decade, average life expectancy has increased. New technologies and medical discoveries have made longer life not just possible, but more pleasant. Not only do we have better cures and maintenance medicines for many diseases once considered an immediate death sentence—we have better ways to detect cancer, heart disease, etc., earlier. And don’t dismiss the importance of mobility. Folks who are mobile live longer—and great strides in joint replacement and prosthetics have allowed folks to maintain greater mobility much longer. A body that moves has a healthier heart. And that innovation likely won’t stop in the period ahead (for reasons covered in Chapter 1). Which means it’s very likely life expectancies keep expanding, and your time horizon should allow for that. And, as said earlier, time horizon is just one key consideration in determining an appropriate long-term asset allocation (i.e., benchmark). It’s an important factor, but not the sole factor and must be considered alongside return expectations, cash flow needs, current circumstances and any other unique personal factors. Which makes determining asset allocation by age and age alone a rule of thumb you can give the boot.